Narrative Over Needlework: Indian menswear’s shift to identity-led retail

5 May 2026, Mumbai

Value is no longer determined by fabric composition, tailoring precision or pricing ladders alone in India’s menswear market today. As the sector moves toward a projected $42.4 billion valuation by 2034, growing at a CAGR of 7.24 per cent from 2026, a new commercial thesis is emerging: emotional resonance is becoming as critical to profits as inventory turns. For decades, menswear was ruled by a product-first formula. Competitive advantage was built through sourcing efficiency, fabric innovation and scale-led distribution. But that logic is weakening as Indian consumers, particularly younger urban cohorts, begin to assess apparel less as a utility purchase and more as a marker of personal identity. In effect, price and value are decoupling.

Retailers across premium and bridge-to-luxury categories are discovering that product proof alone no longer closes the sale. The purchase decision increasingly hinges on whether a brand communicates belonging, aspiration and cultural relevance.

Experience is becoming a financial metric

This shift is visible in the growing performance gap between legacy mass-market retail and identity-led brands.

|

Metric |

Legacy mass-market (avg) |

Identity-driven/d2c (avg) |

|

Footfall Conversion |

12-15% |

22–28% |

|

Customer Retention (12mo) |

18% |

34% |

|

Average Basket Value (ABV) |

Rs 2,800 |

Rs 4,200 |

|

Primary Purchase Driver |

Price/Utility |

Identity/Belonging |

Source: Internal Industry Aggregates, May 2026 Forecasts

The table signals that emotional positioning is translating into hard commercial outcomes. Identity-led brands are converting nearly twice as much store traffic while generating significantly higher basket values, and sustaining stronger retention economics. That matters because retention and repeat spend increasingly determine long-term profitability in a higher customer acquisition cost environment. This is also reframing what store productivity means. So far it was measured through sales per square foot, productivity now increasingly includes lower but monetizable variables, dwell time, engagement intensity, social amplification and community stickiness.

Retailers leading with immersive world-building rather than merchandise density are reportedly generating 2.5 times higher engagement across digital and physical touchpoints. Lighting, soundscapes, curated drops and persona-led merchandising are no longer aesthetic flourishes; they are becoming commercial levers.

The hollowing out of the middle

This evolution is creating pressure on the undifferentiated mid-market, where many legacy players remain exposed. The mass premium segment, long anchored in a value plus aspiration proposition, is being squeezed from both sides. Global fast-fashion players are competing aggressively on trend speed, while Indian D2C labels such as Snitch and Rare Rabbit are winning on sharper cultural signalling.

Large players like Aditya Birla Fashion and Retail are responding through premiumization and designer portfolio expansion, recognising that growth in higher-margin premium categories is increasingly compensating for slower momentum in mass-market formats. What is emerging is less a style war than a redefinition of brand equity. The old commercial equation of quality plus price equals value is giving way to a more layered formula where aesthetic honesty and cultural currency, multiplied by reliability, create brand equity. That is a major departure from traditional retail thinking, because it elevates narrative from marketing function to operating strategy.

When less inventory give more return

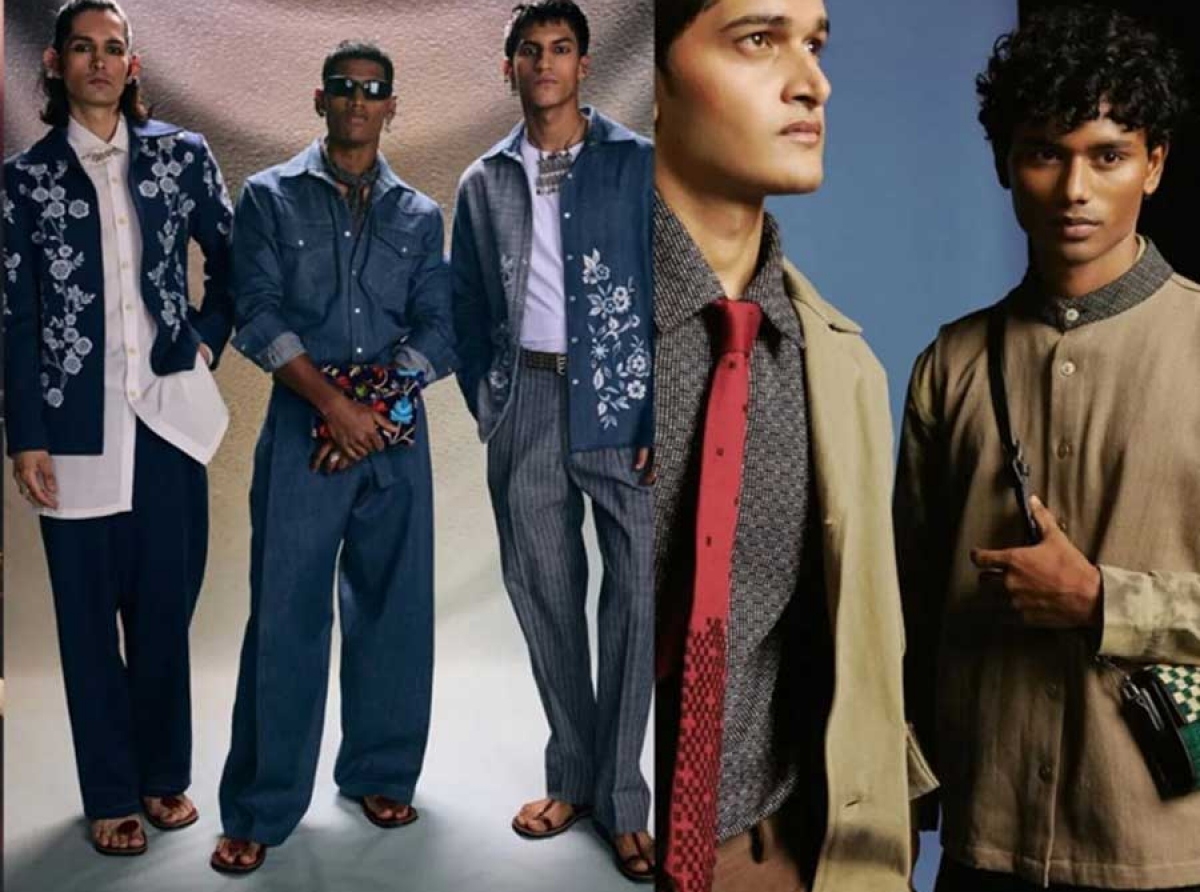

One of the strongest examples of this shift has come through ‘atmospheric ROI’ experiments now appearing across premium retail. A heritage menswear brand’s recent Mumbai pilot that cut floor inventory by 30 per cent in favour of identity-led social hubs and persona zones, offers a revealing template. Rather than pushing assortment breadth, the store organised itself around lifestyle archetypes: the Urban Nomad, Quiet Professional and Cultural Curator. The commercial outcomes challenge orthodox retail assumptions.

Dwell time reportedly rose from 14 to 36 minutes, suggesting emotional engagement can materially increase store productivity. Full-price sell-through improved 19 per cent, indicating stronger brand pull can reduce discount dependency. Organic social mentions rose 400 per cent, effectively lowering blended customer acquisition costs through earned media. The lesson is clear: reducing inventory density did not dilute monetisation; it improved it. That has implications for everything from store design and assortment planning to capital allocation.

Premiumisation finds a new logic

This identity-led turn also helps explain why premiumisation is growing across Indian retail conglomerates. Leaders such as Reliance Retail and ABFRL have long benefited from distribution and multi-brand portfolios, but growth is increasingly shifting toward premium segments where storytelling carries pricing power.

Industry projections suggesting 15-18 per cent annual revenue growth from high-margin premium segments in FY26-27 reflect more than a category upgrade. They signal a structural re-rating of emotional equity as a profit driver. This is particularly relevant as India’s D2C market moves toward a projected $108.7 billion by late 2026, lowering distribution barriers while raising the premium on cultural relevance. In that environment, competitive advantage comes less from access and more from resonance.

The new retail shift is cultural

The larger takeaway for menswear is that identity is becoming a monetizable asset class. Consumers are not merely asking whether a garment fits or lasts. They are evaluating whether a brand reflects who they are or who they aspire to become. That subtle shift is changing what wins in retail. The brands likely to define the next decade may not be those with the deepest inventories or most efficient factories, but those capable of turning emotional relevance into repeatable commercial performance. In that sense, emotional ROI is no longer a soft metric sitting outside the balance sheet. It is beginning to look like the balance sheet itself.